Finding the right auto insurance in Arkansas means balancing state requirements with your personal needs. Here's what you need to know:

- Arkansas Minimum Requirements: Liability insurance with 25/50/25 coverage ($25,000 per person, $50,000 per accident for bodily injury, and $25,000 for property damage).

- Penalties for No Insurance: Fines from $50 to $1,000, registration suspension, and possible jail time for repeat offenses.

- Average Costs: Minimum coverage is about $489/year, while full coverage averages $1,683/year.

- Optional Coverage: Consider comprehensive, collision, uninsured motorist, or gap insurance based on your driving habits and risks.

- Discounts: Save up to 30% with safe driving, anti-theft systems, bundling, or usage-based programs.

- Local Rates Vary: Urban areas like Little Rock are pricier than rural locations like Mountain Home.

Quick Tips:

- Compare multiple quotes using tools like The Zebra or Gabi.

- Adjust coverage based on your car's value and driving habits.

- Take advantage of discounts for safe driving, bundling, or low mileage.

- Review your policy yearly to ensure it meets your needs.

Whether you're a new driver or a seasoned one, staying informed about Arkansas insurance laws and options can help you save money and stay protected.

Get the Cheapest Car Insurance in Arkansas for 2025

1. Know Arkansas Insurance Laws

Understanding Arkansas auto insurance laws is key to selecting the right coverage. The state follows a modified comparative negligence system, which can influence how claims are handled. Here's a breakdown of the rules and potential penalties you should know.

First, familiarize yourself with the 25/50/25 rule, which sets the minimum coverage requirements. Many drivers mistakenly believe this offers comprehensive protection:

While these are the minimums, it's worth noting that full coverage costs an average of $1,683 annually (about $140/month), compared to $489 per year (or $41/month) for minimum coverage [5].

Failure to meet these requirements can result in penalties:

"Understanding Arkansas's car insurance laws is essential for staying compliant and protecting yourself on the road", says Maya Afilalo, Managing Editor & Industry Analyst at autoinsurance.com [5].

To avoid penalties, make sure to:

- Keep valid proof of insurance in your car at all times.

- Maintain continuous coverage without lapses.

- Be ready to show proof of insurance during traffic stops.

- Pay a $100 reinstatement fee if your registration is suspended [6].

"Every automobile owner must have liability coverage. Liability coverage pays for any claims when you are at fault in an accident", Arkansas Insurance Department [1].

Use this information to guide your insurance decisions and stay on the right side of the law.

2. Get Multiple Insurance Quotes

A NerdWallet study highlights notable differences in rates among 18 insurers in Arkansas [7].

When comparing quotes, stick to these recommended coverage limits:

Getting a quote with one of our Martin Agency agents can help you compare quotes efficiently. We provide multi-quote results and can work with you to review your current policy to find potential savings.

When evaluating quotes, keep these factors in mind:

- Coverage Consistency: Ensure all quotes use the same coverage types and limits.

- Payment Options: Compare both monthly and annual payment plans.

- Discount Opportunities: Look into bundling options or other savings programs.

- Specialized Plans: If you drive less often, consider pay-per-mile programs [7].

Be cautious with certain platforms - Insurify requires a phone number, and Compare.com might share your details, which could lead to unwanted contact [8].

For the best rates, combine quotes directly from insurers with trusted comparison tools. Always check privacy policies to avoid unsolicited calls or emails [8].

3. Pick Extra Coverage Types

Optional coverages offer added financial protection beyond the basic requirements, but they do come with higher premiums.

Here are some common options:

In Arkansas, these options are especially relevant due to the state's weather patterns and rural driving conditions.

Why Consider Comprehensive Coverage?

Arkansas drivers often face severe weather risks. Comprehensive coverage can protect you from:

- Tornado damage

- Flood damage

- Hail damage

- Damage caused by falling trees

For Rural Drivers

If you frequently drive in rural areas, pairing Comprehensive and Collision coverages with Roadside Assistance is a smart move. Also, consider higher liability limits to cover unexpected situations.

Making the Right Choice

Think about your car's value, your driving habits, local weather risks, and your financial situation. These factors will help you decide on the right deductibles and coverage limits.

While Arkansas only requires minimum liability coverage, these additional options can save you from hefty out-of-pocket costs in many situations [2][11].

4. Match Coverage to Car Worth

To get the right balance of protection and cost, align your insurance coverage with your car's value.

For newer cars (less than 5 years old), full coverage is often the way to go. It typically costs around $2,670 per year [13] and includes protection for collision, comprehensive, and other non-collision-related risks. However, as your car ages, it might make sense to adjust your coverage. When the cost of full coverage gets close to your car’s market value, it’s time to reassess.

As Your Good Insurance Agency explains:

"Our rule of thumb is that cars valued at $5,000 or less are great candidates for a liability-only policy" [12].

Here’s a quick breakdown of coverage recommendations based on vehicle value:

To decide if full coverage is worth it, follow these steps:

- Check your car's actual cash value using tools like Kelley Blue Book.

- Calculate the annual cost of full coverage, including deductibles.

- Compare the potential claim payout to the total premiums you’d pay.

Here’s an example: A 2010 car might cost $180 per month for full coverage. By dropping collision and comprehensive, that cost could drop to $97 - a 46% savings [14].

Make it a habit to review your coverage regularly, especially if your car's value has dropped or you’re comfortable covering repair costs yourself. Even if you decide to skip comprehensive and collision, it’s smart to keep higher liability limits. In Arkansas, this is essential to protect your assets in case of an accident [13].

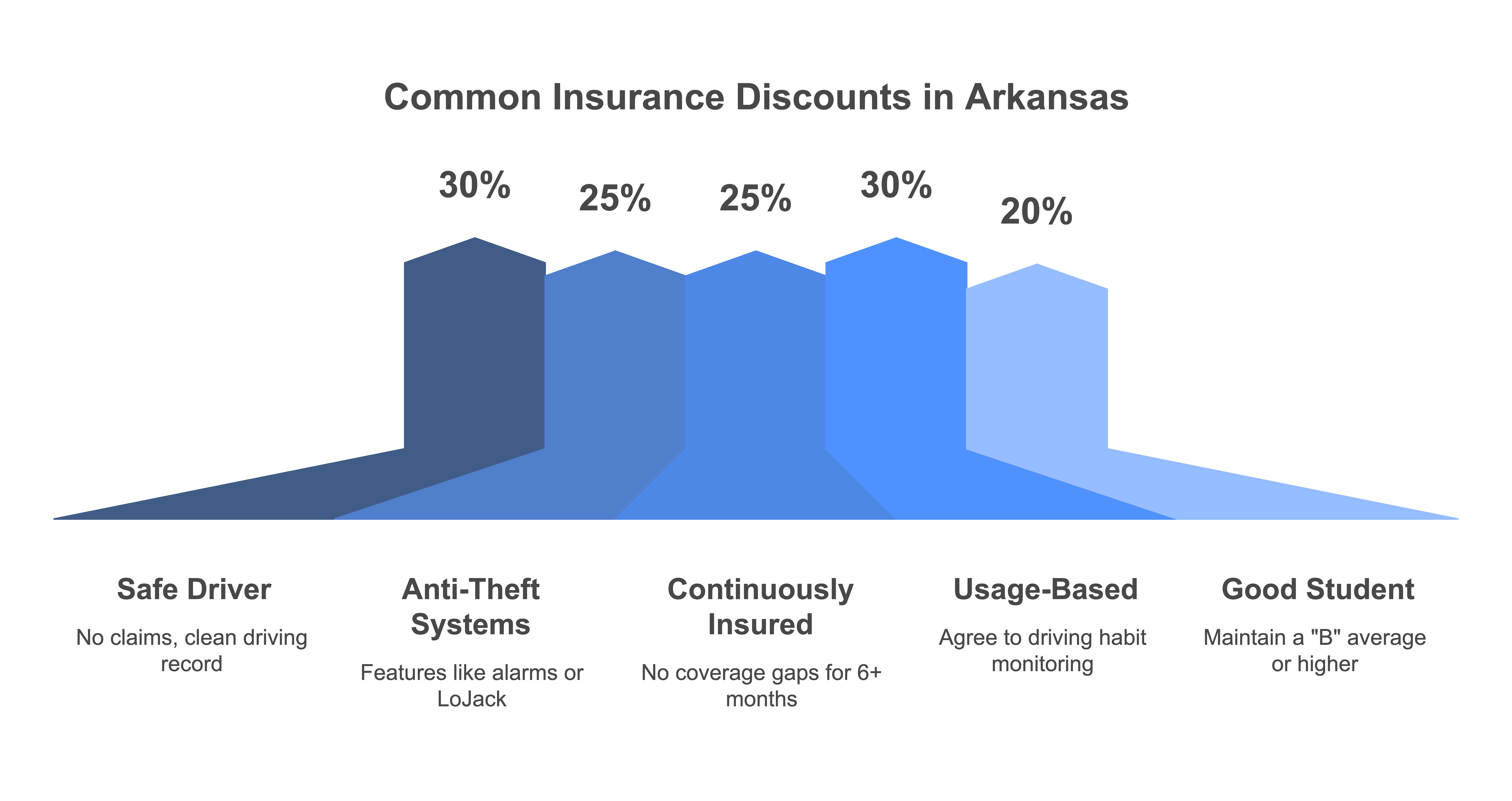

5. Find Arkansas Driver Discounts

Arkansas drivers have several ways to lower insurance premiums, especially by taking advantage of discounts. For instance, maintaining a clean driving record can qualify you for safe driver discounts ranging from 10% to 30% [16].

Here’s a quick look at some of the most common discounts available in Arkansas:

Farm Bureau Insurance, for example, offers a 27% discount if you bundle home and life policies [15]. They also have a special Farm Discount for vehicles used on farms, which is especially helpful for rural residents.

There are other ways to save as well. Completing a state-approved defensive driving course can knock 5% to 10% off your premiums [16]. Arkansas law ensures this discount is available to qualifying drivers.

Modern payment methods like automatic payments and paperless billing can also save you up to 25% [16]. Additionally, check if your job qualifies you for a professional discount, as some occupations can reduce rates.

Lastly, vehicles equipped with safety features like airbags, anti-lock brakes, and daytime running lights can help you save up to 30% [16]. Combining these safety-related discounts with others can significantly lower your overall insurance costs.

6. Check Your Driving Pattern

How you drive and how far you drive each year play a big role in determining your insurance costs in Arkansas. For example, if you drive less than 5,000 miles annually, your average premium might be around $1,678. On the other hand, drivers covering 25,000–30,000 miles annually could be paying a much higher average of $2,304 [17]. The logic here is simple: more miles mean more time on the road, which increases the likelihood of accidents.

Here’s a breakdown of common mileage categories and who typically falls into them:

If you’re a low-mileage driver, you might want to consider pay-per-mile insurance. These plans charge a small amount per mile - typically 5–6 cents - on top of a base monthly fee [17]. As Gregg Barrett, CEO of WaterStreet Company, explains:

"Telematic policies are highly personalized, and for a lot of consumers, that can equal significant savings" [19].

Insurers also look at your driving habits through telematics. Things like speeding or an at-fault accident can increase your rates - sometimes by as much as 50% [20]. To keep track of your mileage, you can use tools like mileage logs, oil change receipts, tracking apps, or even telematics devices.

If you don’t drive much - like remote workers or retirees - ask your insurer how they verify mileage. Providing accurate numbers can help you secure coverage that fits your needs without overpaying. For reference, the national average annual mileage is 13,476 miles [18]. Being upfront about your driving habits ensures you get fair rates and the right type of policy.

7. Research Insurance Companies

When choosing an insurance company, don't just focus on premiums. Companies like USAA, State Farm, GEICO, Auto-Owners, and Shelter each offer different advantages. Evaluating these options helps you find a provider that matches your needs for service quality and local support.

Key Factors to Evaluate

- Financial Stability: Look at AM Best ratings to assess how well an insurer can handle claims. For instance, Auto-Owners' A++ rating highlights its strong financial footing [23].

- Customer Feedback: The NAIC complaint index shows how often customers file complaints relative to the company's size. Auto-Owners stands out with a low 0.50 score, indicating fewer issues compared to competitors [23].

- Claims Process: J.D. Power scores reveal customer satisfaction with claims handling. USAA scores the highest at 879, though it's exclusively for military members and their families [21].

These insights, combined with earlier tips on comparing quotes and coverage, ensure you select a policy that balances cost with service quality.

For those in Arkansas, Martin Agency in Pocahontas offer tailored service and a strong understanding of local needs. If you ever face problems with your insurer, you can file a complaint with the Arkansas State Insurance Department, which works to protect consumers [22].

Finally, check insurer reputations using trusted resources like J.D. Power, AM Best, the NAIC Consumer Insurance Search, and the Better Business Bureau. These tools provide a fuller picture of each company's reliability and service quality.

8. Read Policy Details

Take the time to thoroughly review your insurance policy to avoid unexpected costs or denied claims. In Arkansas, the law requires minimum liability limits of 25/50/25 - that's $25,000 for bodily injury per person, $50,000 per accident, and $25,000 for property damage. However, these limits might not cover all expenses from a serious accident.

For example, if you're involved in an accident with $80,000 in medical bills and $35,000 in property damage, you could still be responsible for up to $40,000 out of pocket [3]. It's also crucial to understand what your policy doesn't cover to avoid surprises later.

Here are some common exclusions:

- Using your vehicle for rideshare, delivery, or racing activities

- Issues related to vehicle condition, like wear and tear, mechanical failures, or modifications

- Damage caused intentionally or during illegal activities

- Driving outside of the country

Once you've reviewed the required limits and exclusions, you might want to explore optional coverage to better fit your needs. For example, Personal Injury Protection (PIP) can help with rehabilitation costs and lost wages, while Uninsured/Underinsured Motorist Coverage protects you if you're hit by a driver without enough insurance.

Keep in mind, Arkansas enforces continuous coverage with a $100 fine for any lapse in insurance [4].

Lastly, familiarize yourself with how to file claims, the documents you'll need, your deductible amounts, and how claims might affect your premiums. Arkansas operates under an at-fault system, meaning the driver responsible for the accident is liable for covering the other party's expenses.

9. Factor in Local Costs

Where you live in Arkansas can have a noticeable impact on your auto insurance premiums. For instance, the average annual cost for full coverage in the state is $1,406 as of 2025 [24]. However, costs can vary significantly between urban and rural areas.

Take a closer look at the differences: residents of Mountain Home pay around $105.82 per month, while drivers in Malvern face $136.50 per month - a gap of over $30 [25]. In Little Rock, full coverage runs 8% higher than the state average, while Bentonville's premiums are 9% lower [27].

Here’s a snapshot of how rates compare in key Arkansas cities:

Insurance rates in Arkansas have also been affected by recent industry changes. Companies have filed rate increases ranging from 5% to 20% [26]. In 2022, insurers paid out 94 cents in claims for every dollar collected in premiums [26]. Local climate risks also play a role in pricing, much like coverage decisions for weather-related damage.

Rural areas tend to offer lower premiums, averaging $1,100 annually, compared to urban areas like Little Rock, where costs can climb to $1,700 [24]. To help manage your insurance expenses, consider these tips:

- Compare rates in different cities if you're planning to move.

- Look into regional discounts, which were covered earlier.

- Adjust your deductible based on local risks.

- Bundle policies with local providers for potential savings.

10. Schedule Policy Reviews

Regularly reviewing your insurance policy is a smart way to ensure your coverage keeps up with your changing needs. Aim to go over your policy every year to make sure it still provides the right protection for your family and assets [28].

Major life events - like getting married, divorced, having a child, your kids starting to drive, retiring, launching a home business, or moving within Arkansas - are also good times for a policy review. Similarly, vehicle-related changes, such as buying a new car, paying off a loan, adding safety features, driving significantly more or less, or making modifications, should prompt a closer look at your coverage. Regular reviews, just like updating your coverage or comparing quotes, help maintain your financial security over time.

Steps for a successful review:

- Gather your current policy and claims history.

- Make a list of any personal or financial changes since your last review.

- Compare your coverage with Arkansas's current insurance requirements.

- Set up a meeting with your insurance agent to discuss adjustments.

- Get updated quotes from several providers to explore your options.

Taking the time to review your policy ensures you're not overpaying and that you're adequately protected.

Conclusion

Choosing auto insurance in Arkansas means meeting the state's legal requirements while addressing your own specific risks and financial situation. Your policy should not only ensure compliance but also align with your personal needs.

Thanks to improved verification systems, the number of uninsured drivers in Arkansas has dropped significantly. However, driving without insurance still comes with serious consequences, including hefty fines and possible jail time. As the Arkansas Insurance Department explains:

"Every automobile owner must have liability coverage. Liability coverage pays for any claims when you are at fault in an accident." [1]

Insurance costs depend on factors like your driving history, credit score, and the level of coverage you select. For example, a strong credit score can help lower premiums, while a DUI can cause rates to spike. It's important to customize your coverage to balance immediate risks with the need to protect your long-term financial assets.

Finding the right policy requires careful research, regular reviews of your insurance, and a clear understanding of how your circumstances impact your coverage. Whether you're new to driving or a seasoned Arkansas resident, staying informed about your options can help you maintain the right coverage while keeping costs manageable.